Gulf Coast Set for Record Natural Gas Pipeline Expansion in 2026

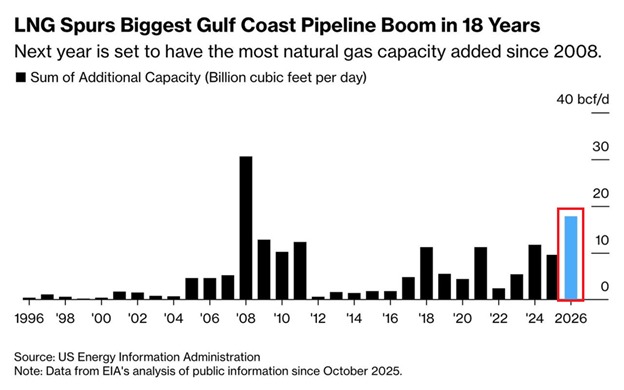

The Gulf Coast is poised to usher in its most expansive single-year addition of natural gas pipeline capacity in 18 years, with roughly 18 billion cubic feet per day (bcf/d) of new infrastructure slated to come online in 2026. The expansion, representing about a 13% increase to the region’s existing pipeline capacity, reflects a concerted push to strengthen LNG export infrastructure as global demand for natural gas surges.

Historical backdrop and scope of the expansion The forthcoming year’s build-out emerges from 12 major pipeline projects scattered across Texas, Louisiana, and Oklahoma. Collectively, these projects aim to move incremental volumes toward LNG terminals along the Gulf Coast, ensuring more reliable supply routes and reducing bottlenecks that have constrained export capacity in recent cycles. Analysts note that the scale of this 2026 expansion is unparalleled since the peak of the shale gas boom around 2008, when the United States witnessed a proliferation of large-diameter pipelines designed to unlock prolific gas plays and feed rising LNG demand abroad.

To put the numbers in perspective, the 18 bcf/d of new capacity would be roughly equivalent to the entirety of Canada’s annual natural gas consumption, underscoring the magnitude of the Gulf Coast’s upgrade. By contrast, earlier expansions in the region tended to add much smaller increments: historical milestones in 2000, 2004, and 2006 typically yielded tens of millions to a few bcf/d, with notable surges occurring during the 2000s but never approaching this year’s scale in a sustained fashion until now.

Driving forces behind the surge Several interlocking factors are propelling the Gulf Coast expansion. First, demand from liquefied natural gas (LNG) exporters has surged worldwide as European and Asian buyers diversify gas supplies and seek energy security in the face of geopolitical tensions and supply disruptions. The Gulf Coast terminals—already among the world’s busiest for LNG loading—benefit from longer-term contracts and a global price environment that keeps LNG competitiveness favorable relative to competing fuels.

Second, domestic gas production on the U.S. mainland has remained robust, supported by tight oil and gas markets, favorable capital conditions, and ongoing infrastructure reinvestments. The new pipelines are not just about moving more gas; they are designed to improve reliability, reduce line pack variability, and provide operational flexibility to handle peak-time demands, maintenance outages, or unexpected supply disruptions.

Third, the expansion reflects a broader strategic objective to maintain the United States’ leadership role in global energy markets. As international buyers seek stable, scalable supplies, the Gulf Coast pipelines are a critical artery, capable of delivering substantial volumes to export terminals while maintaining options for domestic distribution when needed.

Economic implications for the Gulf Coast and beyond The multi-project build-out portends several near- to mid-term economic effects across the Gulf region. Construction activity is expected to generate thousands of jobs, supporting local suppliers, engineering firms, and logistics networks. In the longer run, the enhanced export capacity can contribute to broader regional economic development, including investment in downstream petrochemical sectors that rely on steady feedstock access.

Producers and utility companies along the line expect improved project economics as enhanced transportation capacity can lower marginal costs for gas producers by reducing the risk of constraint-induced price spikes. LNG customers internationally may benefit from more consistent supply, potentially moderating price volatility in regions that have faced acute energy-security concerns.

Regional comparisons and global context The Gulf Coast expansion stands out even when compared with similar developments in other transit corridors. In North America, pipeline capacity growth has been uneven, with some regions incorporating sizable adds during commodity-price cycles and others facing regulatory or environmental permitting challenges. The Gulf Coast, leveraging its established infrastructure, port access, and proximity to major LNG facilities, has historically attracted a disproportionate share of large-scale capacity additions when export demand trends push up global LNG volumes.

Globally, the trend toward LNG diversification and the shift away from single-source energy supply chains have amplified the importance of reliable export conduits. The Gulf Coast projects align with a broader pattern of energy infrastructure investments in North America that aim to stabilize supply routes and enhance export security for a region that plays a central role in global gas markets.

Technical and operational considerations The 18 bcf/d batch of capacity is the product of multiple pipelines, each optimized for different segments of the network. Engineers emphasize that synchronization across pipelines is essential to prevent bottlenecks at interconnections and to ensure that flows can be ramped up or down in response to market conditions, gas-impermeable weather events, or emergency shutdowns at LNG facilities.

Cross-border coordination, though not directly applicable to U.S.-only pipelines, remains a model for how regional pipelines can cooperate with adjacent markets to maximize efficiency and resilience. In practice, operators must navigate safety standards, environmental protections, and community concerns, balancing rapid expansion with responsible siting and mitigation of potential ecological impacts.

Public reception and community impact Public reaction to the expansion has been mixed in some communities along the corridor. Proponents stress the economic benefits, job creation, and energy security advantages, while opponents raise concerns about environmental exposure, noise, land use, and long-term carbon implications. Industry officials and regulators have underscored that modern pipelines incorporate advanced monitoring, leak detection, and rapid shutdown capabilities to minimize risk and to respond swiftly to any operational anomaly.

Investment timelines and project pipelines Industry observers expect the 12 major projects to unfold across a multi-year timeline, with phased commissioning aligned to LNG facility ramp-ups and seasonal demand patterns. The fastest completions could begin to feed into export terminals by late 2025 or early 2026, depending on regulatory approvals, construction progress, and the readiness of auxiliary systems such as compression stations and metering facilities. The overall program is likely to influence capital allocations across the sector, with cautious optimism about achieving planned throughput by the target year.

Environmental considerations and policy context Environmental assessments and permitting processes frame the pace and scope of the expansion. While natural gas is commonly described as a lower-emission bridge fuel relative to coal and oil, the broader climate context continues to shape policy discussions around methane emissions, lifecycle greenhouse gas accounting, and the long-term role of gas in electricity generation and industrial processes. Utilities and pipeline operators emphasize ongoing efforts to reduce fugitive emissions and to invest in monitoring technologies that help quantify and mitigate environmental footprints.

Beyond the surface of infrastructure, industry participants are watching how this expansion interacts with evolving policy signals, including carbon pricing mechanisms, incentives for emissions reductions, and potential mandates tied to cleaner energy transitions. In this sense, the Gulf Coast build-out is not merely a mechanical addition to a pipeline network; it is a barometer of how energy markets adapt to a rapidly changing global energy landscape.

Historical context and the evolution of capacity additions To understand the significance of the 2026 expansion, it helps to recall past episodes of capacity growth. The late 2000s witnessed an unprecedented wave of pipeline construction driven by shale gas development and a surge in natural gas consumption. The subsequent years saw more measured growth, with expansions often tied to regional demand cycles and specific project timelines. The current wave represents a renewed sense of scale, driven by a confluence of domestic production strength and international LNG demand that has kept markets globally interconnected.

Market implications for gas prices and regional dynamics As capacity constraints ease, traders may anticipate shifts in regional pricing dynamics, particularly at hub locations that feed LNG facilities. The ability to move larger volumes more reliably can reduce price volatility during peak seasons or periods of service disruption. However, the ultimate effect on prices will depend on broader supply-demand balances, LNG global demand, and the pace at which alternative energy sources are integrated into the energy mix. In the Gulf Coast, traders will be watching not only local gas prices but also the spread between domestic markets and international LNG benchmarks, which can reflect the region’s growing export capacity.

Public safety, resilience, and long-term planning Long-term resilience planning remains central to projects of this magnitude. Operators are expected to incorporate redundant routes, enhanced compression capacity, and robust maintenance programs to ensure that the system can withstand severe weather events—a critical consideration given the Gulf Coast’s exposure to tropical storms and hurricanes. The industry’s emphasis on resilience will likely shape future regulatory expectations and community engagement strategies, reinforcing the need for transparent communication with residents and businesses along the pipeline corridors.

Conclusion: a pivotal moment for energy infrastructure and global gas markets The 2026 Gulf Coast natural gas pipeline expansion marks a watershed moment for U.S. energy infrastructure and its role in global gas markets. By adding approximately 18 bcf/d of capacity, the region reinforces its position as a central node in the export-oriented LNG system, while also enhancing domestic reliability and price stability. The expansion’s historical scale, aligned with rising international demand and a robust domestic gas base, signals a shift in the energy landscape that could influence policy debates, investment decisions, and regional economic development for years to come.

As construction progresses and commissioning schedules unfold, observers will monitor how the new capacity translates into tangible benefits for producers, LNG customers, workers, and communities along the Gulf Coast. The coming years are poised to test the balance between rapid infrastructure growth, environmental stewardship, and the imperative to provide secure, affordable energy in a rapidly evolving global context.