US M2 Money Supply Jumps by $247.8 Billion in May, Reaching Record $23.1 Trillion

Sharp Monthly Expansion Signals Renewed Liquidity Surge

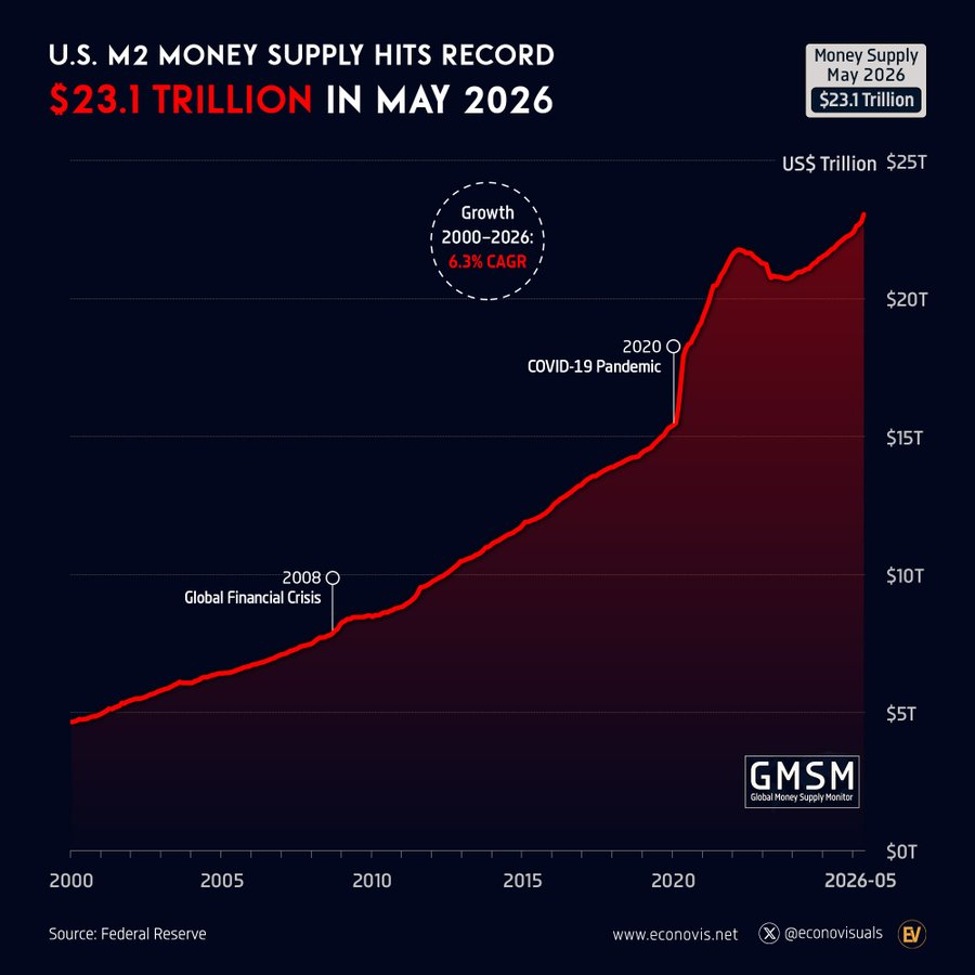

The U.S. money supply posted a significant increase in May, rising by $247.8 billion to reach a record $23.1 trillion. This marks the largest single-month expansion since May 2021, a period characterized by aggressive fiscal stimulus and accommodative monetary policy during the pandemic recovery phase.

The latest data underscores a renewed acceleration in liquidity across the financial system, reversing a period of relative contraction observed through much of 2022 and 2023. On a year-to-date basis, M2 has climbed by $698.6 billion, representing the strongest January-to-May increase in five years.

This sharp rise has drawn attention from economists, market participants, and policymakers, as changes in the money supply are closely linked to economic activity, inflation dynamics, and financial market conditions.

Understanding M2 and Its Economic Role

M2 is a broad measure of the money supply that includes:

- Physical currency in circulation.

- Checking and savings deposits.

- Money market accounts.

- Small-denomination time deposits.

Because it captures both highly liquid cash and near-cash assets, M2 is widely used as an indicator of overall liquidity in the economy. When M2 expands rapidly, it typically signals increased availability of credit and cash, which can stimulate spending, investment, and asset prices.

Conversely, contraction in M2 can indicate tightening financial conditions, often associated with reduced lending and slower economic growth.

Historical Context: From Pandemic Surge to Contraction and Rebound

The current surge in M2 follows a volatile period in U.S. monetary history.

During 2020 and 2021, the money supply expanded at an unprecedented pace as policymakers responded to the economic fallout from COVID-19. Massive fiscal stimulus, combined with near-zero interest rates and large-scale asset purchases by the Federal Reserve, drove M2 growth to historic highs. In some months, increases exceeded $500 billion.

By mid-2022, however, the trend reversed. As inflation surged to multi-decade highs, the Federal Reserve began tightening monetary policy aggressively. Interest rates were raised rapidly, and balance sheet reduction measures were implemented. This shift led to a rare contraction in M2, something not commonly seen in modern U.S. economic history.

The current rebound in 2026 suggests a shift back toward expanding liquidity conditions, though the pace remains below the extraordinary levels seen during the peak pandemic response.

Drivers Behind the Recent Increase

Several factors appear to be contributing to the recent surge in money supply:

- Increased bank lending activity as financial conditions stabilize.

- Rising deposit balances driven by improved household and corporate cash flow.

- Easing financial stress following earlier tightening cycles.

- Potential shifts in Treasury cash management and government spending flows.

Additionally, declining interest rates in certain segments of the financial market may be encouraging movement of funds from higher-yielding instruments back into more liquid accounts included in M2.

While the Federal Reserve does not directly target M2, its policy stance influences the broader financial environment that determines money supply growth.

Inflation Implications and Market Reactions

The resurgence in money supply growth has reignited debate over its potential impact on inflation. Historically, sustained increases in M2 have been associated with upward pressure on prices, particularly when accompanied by strong consumer demand.

However, the relationship between money supply and inflation has become more complex in recent decades due to globalization, technological change, and evolving financial structures.

Recent inflation data has shown signs of moderation compared to earlier peaks, but the renewed expansion in liquidity could complicate the outlook if it translates into increased spending.

Financial markets have responded cautiously. Equity markets often benefit from higher liquidity, as increased cash availability can support asset valuations. Meanwhile, bond markets may react to expectations of future inflation or shifts in monetary policy.

Regional and Global Comparisons

The United States is not alone in experiencing shifts in money supply dynamics, though its scale remains distinctive.

In the eurozone, money supply growth has been more subdued following aggressive tightening by the European Central Bank. M3, the European equivalent of M2, has shown slower expansion and, at times, contraction in recent years as policymakers prioritized inflation control.

In contrast, some emerging markets have experienced more volatile money supply trends, driven by currency pressures, capital flows, and domestic policy adjustments. Countries with less stable financial systems often see sharper swings in liquidity, which can translate into higher inflation volatility.

Japan presents a different case. Despite long-standing accommodative monetary policy, money supply growth has been relatively steady, reflecting structural factors such as demographic trends and persistent low inflation.

Compared to these regions, the U.S. continues to exhibit a more dynamic and responsive monetary environment, with sharper expansions and contractions tied to policy shifts and economic cycles.

Impact on Households and Businesses

Changes in the money supply can have tangible effects on everyday economic activity.

For households, increased liquidity often translates into easier access to credit, more stable income flows, and greater spending capacity. This can support consumption, particularly in sectors such as housing, retail, and services.

For businesses, rising money supply can lower borrowing costs and improve access to financing, enabling investment in expansion, hiring, and innovation.

However, if money supply growth outpaces economic output, it can contribute to inflationary pressures that erode purchasing power. This creates a delicate balance for policymakers seeking to sustain growth while maintaining price stability.

Banking System and Credit Conditions

The recent increase in M2 also reflects evolving conditions within the banking system.

Deposit growth has stabilized after a period of outflows linked to higher interest rates and competition from alternative savings instruments. Banks appear to be regaining footing, with improved balance sheets and more consistent lending activity.

Credit conditions have gradually eased, particularly for large corporations and well-qualified borrowers. However, lending standards remain relatively tight in certain sectors, including commercial real estate and small business financing.

The interplay between deposit growth, lending activity, and regulatory factors will continue to shape the trajectory of the money supply in the coming months.

Policy Outlook and Uncertainty

The Federal Reserve faces a complex environment as it assesses the implications of rising money supply.

While M2 is not an official policy target, its growth can influence broader economic conditions that inform interest rate decisions. Policymakers must weigh the benefits of increased liquidity against the risk of reigniting inflationary pressures.

Key questions moving forward include:

- Whether the current surge represents a sustained trend or a temporary fluctuation.

- How increased liquidity will interact with consumer spending and wage growth.

- The extent to which global economic conditions will influence domestic money supply dynamics.

Uncertainty remains elevated, particularly given ongoing shifts in global trade, geopolitical developments, and technological change.

Looking Ahead: Signals to Watch

As the year progresses, analysts will closely monitor several indicators to assess the impact of rising M2:

- Inflation trends, particularly core measures that exclude volatile components.

- Consumer spending patterns and retail activity.

- Credit growth across households and businesses.

- Financial market responses, including equity and bond performance.

The trajectory of the money supply will also depend on broader economic momentum. Strong growth could absorb increased liquidity without triggering significant inflation, while weaker conditions could amplify its effects.

The latest data highlights a renewed expansion in U.S. liquidity, marking a notable shift after a period of tightening. Whether this trend evolves into a sustained cycle or remains a short-term development will play a critical role in shaping the economic landscape in the months ahead.