Foreign Holdings of US Treasuries Fall Sharply in March: Global Shifts in Demand and Their Economic Ripples

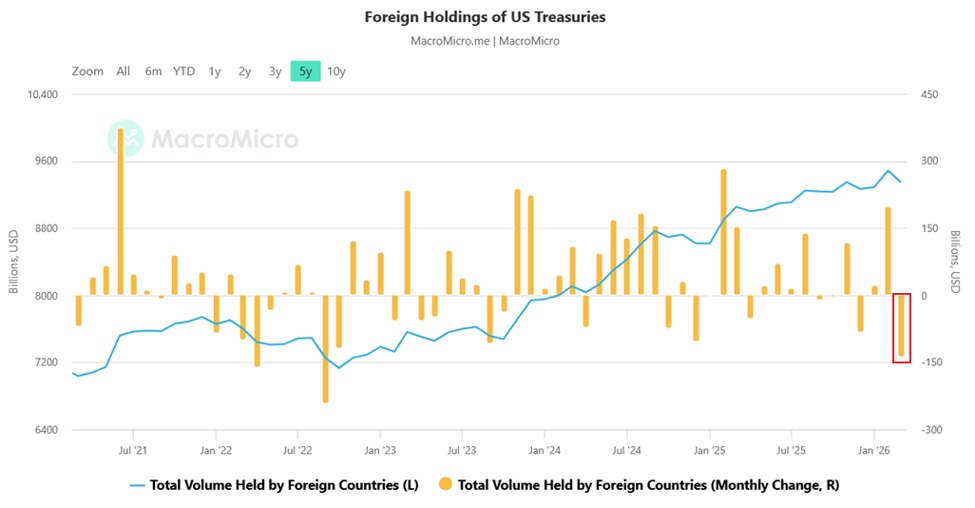

A pronounced shift in the global appetite for US government debt unfolded in March, as foreign holdings of US Treasuries declined by $139 billion to $9.35 trillion. This marked the steepest monthly drop since September 2022 and underscored evolving dynamics among major holders of American government bonds. The data, released by the Treasury Department, reflect a confluence of policy actions, currency management strategies, and broader macroeconomic currents that collectively shape the path of global finance in the months ahead.

Historical context: how we arrived at March’s numbers To understand the March drop, it helps to recall the longer arc of foreign sovereign demand for US Treasuries. The United States has long benefited from a deeply liquid, creditworthy market, attracting buyers from around the world seeking safety and predictable yields. Over the past decade, foreign holdings have ebbed and flowed with shifts in foreign exchange reserves, interest-rate expectations, and geopolitical risk assessments. The March decline arrives after a period in which several large holders rebalanced their portfolios or adjusted reserve strategies in response to domestic monetary policy and currency considerations.

Japan’s portfolio reallocation: currency defense and fiscal balance Japan, historically the largest foreign holder of US Treasuries, reduced its holdings by $48 billion in March, bringing its total to $1.19 trillion—the lowest level since December 2025. Analysts point to a confluence of factors behind Japan’s move. The Bank of Japan’s ongoing interventions to support the yen, aimed at stabilizing a depreciating currency and mitigating import-driven inflation, require both tactical reserve management and strategic cross-currency considerations. While the yen’s value has experienced volatility, Japan’s central bank has emphasized a cautious approach to intervention, seeking to balance domestic inflation pressures with the need to maintain foreign-exchange stability. The reduction in US Treasury holdings fits into a broader pattern of adjusting foreign-exchange reserves rather than a wholesale shift away from dollar-denominated assets. For policymakers, this development underscores how currency defense operations can influence the composition of official reserves, with implications for cross-border capital flows and the functioning of the dollar funding markets.

China’s continued de-dollarization: a structural pullback China’s holdings of US Treasuries declined by $41 billion in March to $652 billion, reaching the lowest level since September 2008. This marks a continuation of a longer-term trend in which Chinese reserve managers have diversified away from US debt amid concerns about US fiscal dynamics, increasing geopolitical frictions, and a desire to diversify reserve holdings beyond the dollar-centric framework. Since the start of 2025, China’s Treasury holdings have fallen by about $109 billion, a roughly 14% retreat. Observers note that China’s strategy has included diversifying into other assets, including commodities, alternative currencies, and domestic investment channels, while maintaining a substantial but reduced stake in Treasuries. The March data thus reflect not an abrupt pivot away from dollar assets, but a gradual, strategic reallocation shaped by risk management, domestic growth aims, and a calculus about future US interest-rate trajectories.

The United Kingdom’s notable rise: a shift in reserve strategy In contrast, the United Kingdom increased its holdings by $30 billion in March, reaching a record $927 billion. The UK’s treasury management and central banking framework has prioritized liquidity and safety within the gilt market, albeit within a broader global context of currency volatility and inflation dynamics. The UK’s escalation of US Treasury holdings suggests a deliberate preference for diversification within dollar-denominated reserve assets, even as other major holders trim exposure. This behavior may reflect strategic positioning in response to shifts in the relative attractiveness of US Treasuries versus other safe-haven assets, as well as the longer-term expectations for US fiscal policy, inflation, and interest rates.

Other notable trends: who bought, who sold, and what it means

- The data show a mixed bag of moves among other buyers and sellers. While thenumbers highlight the declines by Japan and China and the rise in UK holdings, several smaller holders and central banks have also adjusted their portfolios in the wake of evolving risk assessments and currency considerations.

- Market participants often interpret these movements as a signal of shifting demand for US debt as a global funding instrument. When major holders reduce their positions, liquidity in the US Treasury market can become more sensitive to shifts in domestic demand, including that of pension funds, insurance companies, and international banks seeking safe assets.

- The broader context includes domestic American monetary policy. The Federal Reserve’s approach to inflation, interest-rate signaling, and balance-sheet normalization can influence foreign appetite for Treasuries. If US yields are expected to rise, foreign holders may reassess the relative attractiveness of longer-term securities versus shorter maturities or other asset classes.

Economic impact: ripple effects across markets and policy considerations The March decline in foreign holdings has several potential economic implications:

- Funding costs and the yield curve: Foreign demand helps anchor Treasury prices and influence borrowing costs for the US government. A notable reduction in foreign demand could exert upward pressure on yields, especially if domestic buyers do not fully offset the selling. An upward shift in yields can influence mortgage rates, corporate borrowing costs, and overall financial conditions in the United States.

- Currency markets and reserve management: Central banks manage their currency reserves with an eye toward diversification, liquidity, and risk management. Shifts in Treasury holdings can reflect broader rebalancing strategies that affect exchange rates, carry trade dynamics, and bilateral financial relationships. Countries like Japan and China calibrate reserves not only for security but also for macroeconomic objectives such as inflation targeting and growth stimulation.

- Global funding stability: The stability of the US Treasury market is a linchpin for global finance. A durable pattern of shifting demand could prompt policymakers and market participants to explore hedging and risk-management strategies, including increased use of swap lines, liquidity facilities, and cross-border collaboration to ensure smooth funding channels.

Regional comparisons: how different markets fit into the picture

- East Asia: Japan’s reductions alongside China’s retreat reflect a broader regional recalibration of reserve portfolios in response to domestic policy priorities and global risk assessments. While both nations trimmed holdings, the pace and magnitude vary, signaling nuanced approaches to currency stability and strategic asset allocation.

- Europe: The UK’s sensitivity to global yield movements and its willingness to accumulate more US Treasuries may reflect a preference for structural safety in a volatile environment. European central banks and sovereign funds often balance Treasuries with euro-denominated assets and diversification across geographies.

- North America: Canada and other North American institutions typically adjust Treasury holdings in line with domestic monetary policy expectations and trade considerations. The March data highlight the interdependencies of North American financial markets within a global system anchored by the US dollar.

What this means for investors and the public

- For investors, the March data underscore the importance of monitoring foreign demand trends as a factor in liquidity and yield expectations. A reduction in official holdings may lead to tighter liquidity in certain tenors or more pronounced sensitivity to domestic demand fluctuations.

- For policymakers, the shifts highlight the need to consider currency dynamics, reserve strategy, and the potential feedback effects on inflation and growth. While Treasury debt remains a safe, liquid asset, shifts in its composition are a bellwether of global risk appetite and macroeconomic posture.

- For the general public, the implications are indirect but meaningful. Changes in Treasury yields can influence mortgage rates, student loan costs, and other credit conditions that affect household finances. The broader narrative remains the resilience of a deeply integrated financial system that relies on the reliability of US debt markets.

Historical context: long-standing factors shaping demand for US debt Over decades, foreign holdings of Treasuries have oscillated in response to:

- Monetary policy expectations in the United States, including anticipated path of interest rates and inflation.

- Foreign exchange reserve management, with central banks seeking safety, liquidity, and diversification.

- Geopolitical developments and risk sentiment, which sway demand for perceived safe-haven assets.

- Domestic fiscal policy and long-term debt outlook, which influence the relative attractiveness of US debt versus other instruments.

In this March snapshot, the confluence of currency-management actions by major holders, coupled with ongoing diversification efforts, created a moment that drew attention from financial markets, policymakers, and observers worldwide. While no single factor dictates the outcome, the aggregate effect is a clearer picture of how global holdings of US Treasuries respond to a shifting mix of policy priorities, risk tolerances, and economic forecasts.

Looking ahead: cautious optimism amid continued resilience Analysts expect that the US Treasury market will continue to display resilience even as foreign demand retrenches in part. The United States remains the issuer of the deepest, most liquid debt market, with a long track record of capacity to absorb shifts in demand. Domestic buyers, including pension funds, mutual funds, and other institutional investors, will likely adapt to evolving supply dynamics, potentially adjusting duration, credit exposure, and hedging strategies.

The global economy’s trajectory—riding on inflation, growth, and currency stability—will continue to influence how foreign holders calibrate their portfolios. If inflation pressures ease and economic activity strengthens, US yields may stabilize, providing a balanced backdrop for both foreign and domestic investors. Conversely, if inflation persists or if global risk sentiment deteriorates, demand patterns could become more volatile, triggering broader shifts across asset classes that rely on US Treasury funding.

Final reflection: a moment of transition in a durable system The March decline in foreign holdings of US Treasuries serves as a reminder that even the most established financial architectures are subject to adaptation. The United States’ debt market remains a cornerstone of global finance, but the composition of its owners—government reserves, financial institutions, and international investors—continues to evolve. As Japan, China, the United Kingdom, and other participants recalibrate their portfolios, market observers watch for signs of how these shifts translate into interest rates, currency trajectories, and the flow of capital across borders.

In summary, March’s Treasury data highlight a pivotal moment of rebalancing among the world’s major holders. The numbers reflect a complex interplay of currency defense, diversification, and strategic asset allocation. For businesses, policymakers, and everyday savers alike, the implications extend beyond a single month, offering a lens into how global finance negotiates risk, safety, and opportunity in an interconnected world.