Precious Metals Market Faces Sharp Declines Amid Lingering Volatility

A broad-based slide swept through precious metals markets on Monday, with all major metals retreating to fresh daily lows. The retreat comes after a period of renewed volatility in the sector, underscoring the delicate balance between safe-haven demand and shifting macroeconomic signals that influence investor sentiment.

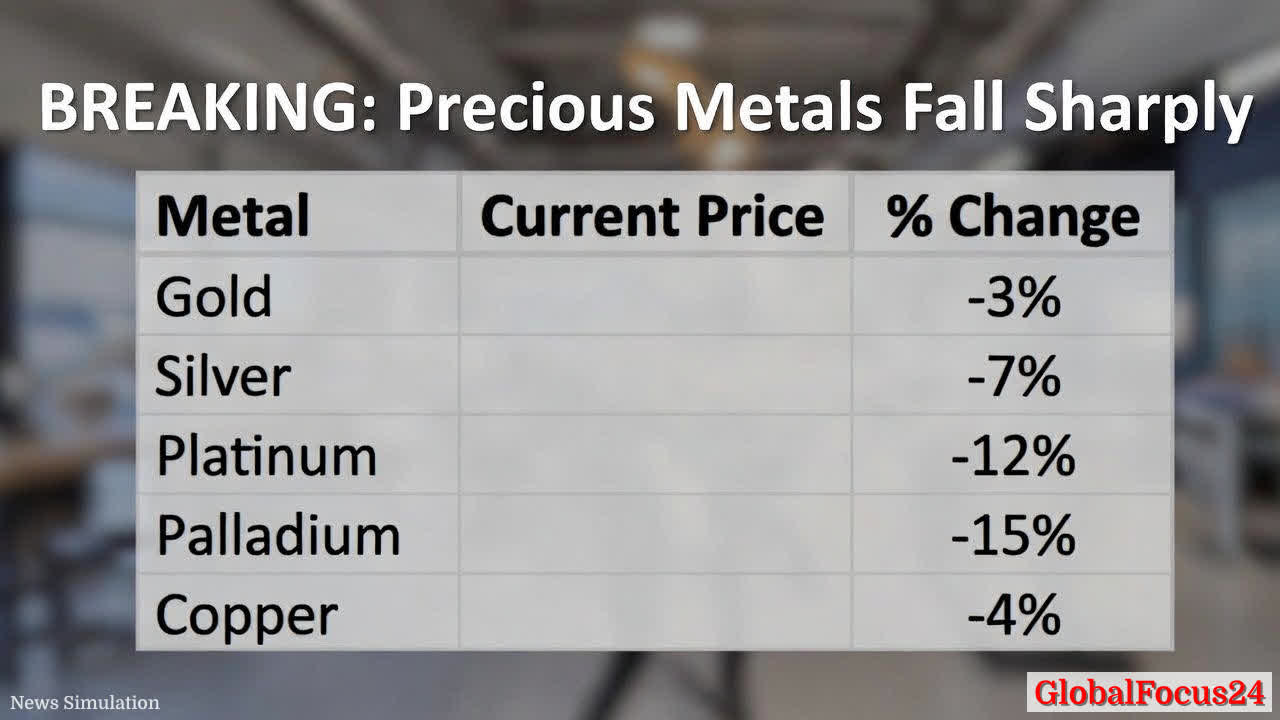

Market snapshots and immediate implications Gold led the declines, retreating about 3% to around $4,420.70 per ounce after a intraday dip of roughly $132.00. The yellow metal’s move reflects a combination of stronger U.S. dollar dynamics, a turning of interest-rate expectations, and shifting risk appetite among institutional and retail investors. While gold has historically been viewed as a hedge against uncertainty, recent price action suggests a more nuanced relationship with prevailing macro factors, including inflation trajectories and real yields.

Silver posted a softer performance, down roughly 7% to about $72.25 per ounce following a $4.95 fall. The broader silver complex often moves with industrial demand as well as investor flows, and today’s decline indicates a temporary loosening in industrial demand concerns alongside a cautious macro outlook.

Platinum experienced a steeper decline of around 12%, trading near $2,206.95 per ounce after a $284.15 drop. Platinum’s sensitivity to global auto-sector demand—particularly for catalytic converters—means its price can act as a proxy for broader manufacturing activity and supply-side constraints within key producing regions.

Palladium registered the steepest percentage decline, slipping about 15% to around $1,736.25 per ounce after a $315.65 fall. Palladium’s path has been closely tied to automotive demand, and a downturn in this metal often mirrors shifts in vehicle production forecasts, geopolitical risk premiums, and substitution dynamics with other platinum-group metals.

Copper, a bellwether for global economic health, decreased by roughly 4% to about $5.62 per pound after a $0.22 reduction. The copper complex often moves with broader industrial activity indicators, including manufacturing PMIs, construction demand, and international trade flows. Today’s weakness points to a cautious outlook for commodity-intensive sectors in the near term.

Historical context: cycles of risk, safety, and stimulus The current pullback sits within a longer history of how precious metals respond to evolving economic landscapes. In times of acute stress or geopolitical tension, investors frequently flock to perceived safe-haven assets, with gold and, to a lesser extent, silver and platinum group metals seeing price strength. Conversely, periods of growing economic confidence, rising real yields, or a strong U.S. dollar can weigh on precious metals as investors reallocate toward higher-yielding assets.

Over the past decade, several notable cycles have demonstrated that metal prices can experience sharp swings even when underlying fundamentals—such as supply constraints or demand trends—remain relatively stable. This dynamic often reflects the rapid re-pricing of risk, the influence of central bank signaling, and the evolving interplay between financial markets and real-economy indicators.

Regional performance and comparisons Historically, regional drivers can amplify or dampen global metal movements. In Asia, for example, industrial activity, import demand, and local currency dynamics can magnify price shifts, particularly for metals with large industrial applications. Europe’s metal markets tend to reflect a mix of manufacturing momentum, energy costs, and policy signals that can influence both demand and substitute patterns. North American markets frequently respond to domestic monetary policy expectations, energy price shifts, and infrastructure-related demand.

When comparing regional patterns, it is common to see timing differences in price responses to macro news. For instance, a strong rally in one region can be tempered by softer data elsewhere, creating a cross-border price mosaic rather than a single, uniform trend. In today’s session, the broad-based declines indicate a global recalibration rather than a localized hiccup, suggesting the market is weighing near-term macro risks against the broader longer-term unwind or reallocation strategies.

Economic impact and broader market implications For producers and consumers, the move lower in precious metals prices can influence hedging strategies, investment decisions, and production economics. Mining companies might experience changes in revenue volatility and project economics, particularly for margins tied to precious metal byproducts. Jewelry and industrial users may see nuanced effects, as price volatility can complicate procurement planning, inventory management, and cost control.

From a financial markets perspective, the metal complex often serves as a barometer for risk sentiment and inflation expectations. A sharp, broad-based decline can signal a reassessment of inflation volatility, the pace of central-bank normalization, or appetite for alternative assets. Portfolio managers may respond by reevaluating exposure to bullion-backed exchange-traded products, futures, and other derivatives that offer liquidity and diversification in turbulent times.

Geopolitical and macro considerations Geopolitical developments, trade dynamics, and global growth trajectories continue to shape metal prices. In periods of heightened geopolitical risk, safe-haven demand for gold can intensify, while industrial metals like copper and palladium respond primarily to manufacturing activity and supply chain resilience. The precise balance between these forces varies with the news cycle, economic data releases, and policy announcements, making daily moves in the metal complex both pronounced and highly sensitive to new information.

Market participants are closely watching inflation trajectories, wage growth, and consumer demand signals as they assess the trajectory of real interest rates. Even modest shifts in expectations for rate hikes or cuts can translate into outsized moves for metal prices, given their sensitivity to the opportunity cost of holding non-yielding assets.

Sustainability, supply, and longer-term outlook Supply-side considerations, including mine production levels, recycling rates, and geopolitical risks in key mining regions, will continue to factor into the longer-term outlook for precious metals. Environmental, social, and governance (ESG) considerations increasingly influence investment flows, with funds incorporating sustainability criteria into allocation decisions. In the near term, price volatility may persist as markets accumulate new information about demand resilience, inventory levels, and policy directions.

Investors and analysts are likely to reassess scenarios where demand outpaces supply in certain metals while others face structural oversupply conditions. The evolving substitution dynamics—where one metal might partially replace another in industrial applications—could also shape price trajectories over the medium term.

Public reaction and sector sentiment Market reactions to the latest declines have been varied. Some investors view the pullback as a potential buying opportunity, citing historical rebounds following corrections and the ongoing uncertainty surrounding inflation and growth dynamics. Others remain cautious, emphasizing that further volatility could persist if macro data disappoints or if policy signals shift unexpectedly. Analysts note that sentiment in the precious metals market often shifts quickly in response to new data on inflation, monetary policy, and global risk events.

Regional comparisons reveal that while price declines are widespread, the degree of impact differs among market participants. Retail buyers may adjust purchases as prices retreat, while institutional traders re-balance portfolios to manage risk and maintain liquidity. The collective mood reflects a market attuned to a broad set of economic indicators rather than a single driver, underscoring the complexity of forecasting in a domain where fundamentals intersect with sentiment.

Conclusion: navigating a volatile landscape Today’s broad-based declines across gold, silver, platinum, palladium, and copper underscore the ongoing volatility in the metals sector. As markets digest evolving macro signals, participants will monitor inflation trends, central-bank policy expectations, and global production data to gauge the next moves. While the short-term path remains uncertain, the longer-term outlook for precious metals will continue to depend on the balance between safe-haven demand, industrial demand, and the cost of capital in a shifting global economy. Investors, policymakers, and industry players alike are urged to track market signals closely, hedge appropriately, and maintain a disciplined approach to risk management in a environment characterized by rapid information flow and dynamic price discovery.