Trump Bans Institutional Purchases of Single-Family Homes, Shifting US Housing Market Dynamics

A sweeping policy aimed at curbing institutional consolidation in the United States housing market has sparked a broad conversation about affordability, supply, and long-term economic resilience. The administration announced measures prohibiting large institutional investors from acquiring additional single-family homes, signaling a strategic shift in how the country approaches housing access for middle- and working-class households. The move arrives amid mounting concerns about the role of big investment firms in reshaping neighborhood dynamics, price trajectories, and the availability of homes for individual buyers.

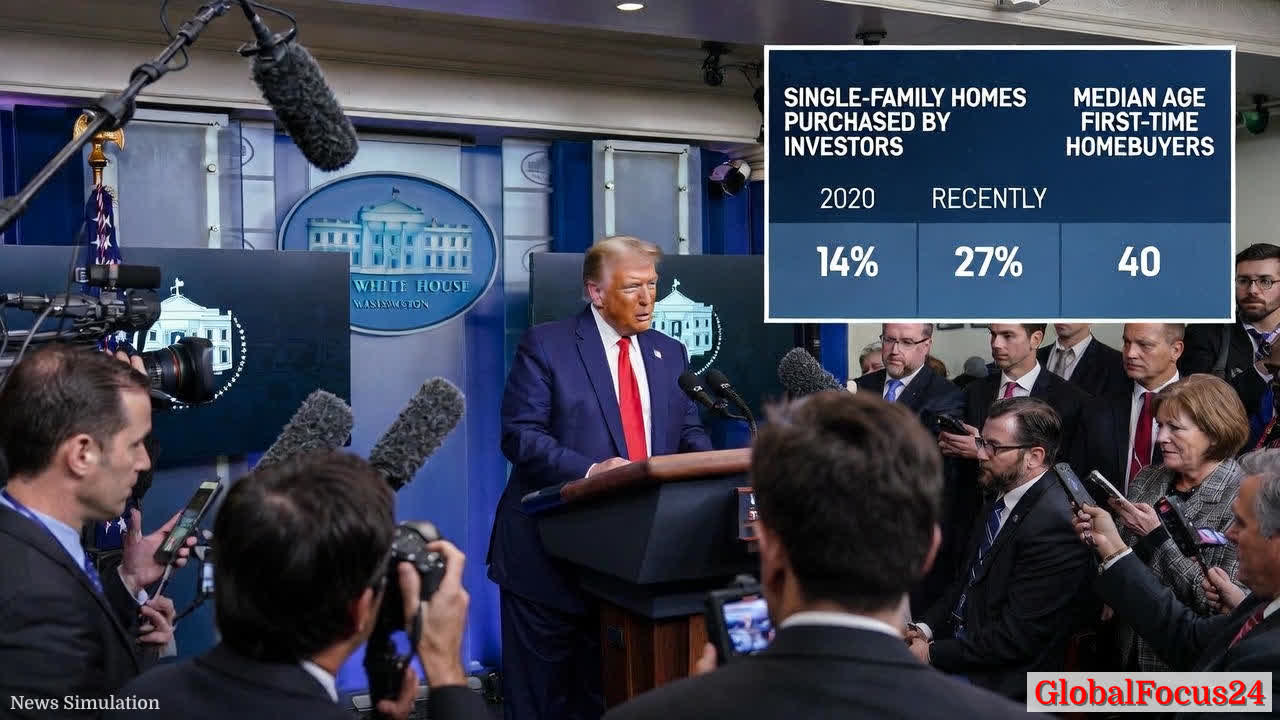

Historical context: how we arrived here The United States has long balanced incentives for homeownership with market-driven housing supply. Over the past decade, however, a convergence of factors—rapid urbanization, zoning rigidity, limited new construction, and historically low mortgage rates—created conditions where investors could leverage scale to purchase and hold properties. In the wake of the 2008 financial crisis, policy makers emphasized stabilizing the housing market, while the pandemic era introduced a temporary but transformative shift in demand patterns. As households sought flexibility and security, investors, including real estate investment trusts and private equity platforms, expanded their footprint in single-family rental markets. By the midway point of the 2020s, investor activity in single-family transactions had risen markedly, raising questions about the accessibility of ownership for first-time buyers and families seeking stable housing.

Economic implications: beyondnumbers The policy aims to address a core economic tension: the affordability of homeownership in a climate of supply constraints. Housing cost burdens have broad consequences for consumer spending, savings, and long-term wealth accumulation. If fewer households can transition from renting to owning, the economy could experience slower household formation, reduced spending on durable goods, and delayed wealth-building for millions of families. Conversely, proponents argue that directing capital toward diversified housing strategies could stabilize neighborhoods and promote rental housing quality, potentially offering temporary relief for renters.

Regional comparisons illuminate a nuanced landscape. In markets with high housing turnover yet limited new supply—such as several Sun Belt cities and fast-growing metropolitan areas—institutional acquisitions have been a more visible feature of the market. In contrast, locales with more robust development pipelines and denser zoning, like certain midwestern hubs, have demonstrated greater elasticity in response to policy shocks that affect investor activity. The net effect of the ban will likely vary by region, depending on existing stock, rental market dynamics, and local policy environments.

Mechanisms and scope: what the policy covers The administration’s action targets future acquisitions by large institutional entities, with criteria designed to distinguish between individual homebuyers and organizations that acquire homes at scale. Existing investor-owned portfolios are not retroactively affected by the measure. By focusing on new purchases, the policy seeks to deter excessive market concentration while preserving the ability of existing owners to manage their investments, and it leaves room for ongoing rental markets to operate with a mix of ownership structures.

Market response and behavioral shifts Financial markets reacted with heightened scrutiny of real estate equities and related assets. The response from major players in the housing finance ecosystem has included reassessment of investment models, hedging against policy risk, and an accelerated emphasis on supply-side strategies. Real estate developers and construction firms might adjust project timelines in anticipation of changes in demand dynamics. Mortgage lenders may also recalibrate underwriting criteria if anticipated changes in ownership patterns influence credit risk and borrower profiles.

The supply-side narrative dominates expectations for medium-term outcomes. Analysts highlight that structural bottlenecks—such as permitting delays, land-use restrictions, and long lead times for new construction—continue to constrain the pace at which new homes reach the market. Even with reduced investor demand, the fundamental constraint appears to be supply, rather than demand alone. In such a context, policy measures that improve land use efficiency, streamline approvals, and incentivize affordable housing could play a more decisive role in restoring balance.

Impacts on households and neighborhoods For many aspiring homeowners, the policy could translate into greater entry opportunities, at least in theory, by reducing competition from buyers with substantial capital backing. This could ease price pressures for some properties in markets with acute affordability challenges. Yet the degree of impact is contingent on how quickly new listings and affordable units become available, as well as the responsiveness of sellers to shifting demand dynamics.

From a neighborhood perspective, concerns about investor-driven homogenization—where single-family rental profiles replace long-standing owner-occupied communities—remain a focal point of public discourse. Proponents of the policy argue that improving access to homeownership supports stable, locally rooted communities, while critics caution that rental housing quality and availability must be safeguarded to prevent unintended dislocations or price volatility in rental markets.

Historical precedents and policy trajectories Comparisons with past housing cycles reveal that supply responsiveness often determines the ultimate effectiveness of demand-side interventions. When policymakers have anchored reforms to supply expansion—such as easing zoning restrictions, financing options for developers, and incentives for affordable construction—the resulting dynamic tends to be more durable than measures aimed solely at demand suppression. The current approach, while addressing concerns about market concentration, may benefit from a complementary set of supply-oriented policies to maximize its stabilizing potential.

Policy design considerations: balancing interests Key design questions revolve around scale, enforcement, and transitional timelines. How large must an investor be to trigger the policy’s restrictions? What constitutes an acquisition in the context of joint ventures, private equity, and publicly traded real estate vehicles? How will enforcement be monitored, and what penalties will apply for non-compliance? Establishing clear, predictable rules can reduce market uncertainty and help investors reroute capital toward productive uses that support housing affordability, such as community land trusts, co-ops, and innovative financing models.

The role of public-private collaboration in expanding supply A successful path forward likely rests on collaboration among federal, state, and local authorities, private developers, and community organizations. Public-private partnerships can harness private capital for affordable housing while ensuring that developments align with community needs. Streamlined permitting, flexible zoning for missing middle housing, and targeted subsidies for low- to moderate-income households can complement demand-side measures, creating a more resilient and inclusive housing ecosystem.

Public sentiment and social dimensions Public reaction to housing policy tends to reflect a mix of urgency and optimism. Homeownership remains a defining milestone for many families, and any policy that promises a pathway back toward affordability resonates broadly. At the same time, concerns about rental market stability, neighborhood character, and the speed of construction deployment persist. Effective communication about the policy’s goals, safeguards, and expected timelines will be crucial to maintaining public trust and ensuring smooth implementation.

Economic ripple effects and long-term outlook In the near term, the policy could influence capital allocation strategies across real estate and construction sectors. Lenders, developers, and investors may recalibrate project pipelines, potentially prioritizing affordable housing and mixed-income developments. Over the longer horizon, a more favorable balance between supply and demand could help stabilize home prices and reduce fluctuations driven by speculative activity. The ultimate measure of success will be whether households can access affordable pathways to ownership without compromising market efficiency or investor viability that supports economic dynamism.

Concluding perspectives The housing market remains a mosaic of demand, supply, policy, and opportunity. The decision to restrict institutional acquisitions of single-family homes represents a deliberate pause in a rapid transformational trend, paired with a broader commitment to addressing affordability and market balance. While the path to meaningful, enduring change requires sustained, multi-faceted effort—combining demand moderation with aggressive supply-side reforms—the policy signals a clear intent: to re-center housing accessibility within the aspirations of ordinary families and communities across the nation.

Notes for readers

- The housing affordability crisis is underscored by a price-to-income ratio that exceeds historical norms in several regions, signaling structural pressure on household budgets.

- Existing owner households continue to benefit from historically low mortgage rates relative to current levels, shaping selling decisions and market dynamics.

- As new housing starts and completions respond to policy signals, regional variations will define the pace and character of market adjustments.

Public interest and future considerations Stakeholders will be watching for how quickly housing supply expands, how rental markets adapt to changing ownership patterns, and how policymakers balance investor protections with the need to foster a dynamic, innovative housing industry. The coming years may reveal whether this policy serves as a catalyst for more affordable ownership opportunities, or whether it highlights the necessity of complementary reforms to solve deeper structural bottlenecks in housing production and distribution.