U.S. Graduate Programs Face Sharp Decline in International Student Enrollment in 2025

A Sudden Shift After Years of Growth

International student enrollment in U.S. higher education experienced its first overall decline in three years during the fall of 2025, signaling a potential turning point for American universities that have increasingly relied on global talent. According to newly released data from the National Student Clearinghouse, total international enrollment dropped 1.4% from the previous year—equivalent to roughly 5,000 fewer students nationwide.

Most notably, the decline was concentrated at the graduate level, where enrollment fell by a striking 6%, or about 10,000 students, marking the sharpest contraction in at least five years. The downturn reverses a four-year streak of robust growth that had seen international graduate enrollment rise nearly 50% between 2020 and 2024.

For many universities—especially large public research institutions—this shift represents both a financial and academic challenge. The data show that public four-year universities faced a particularly steep 9% drop in graduate international students, underscoring the sector’s vulnerability after years of steady expansion.

Understanding the Numbers: A Reversal in Momentum

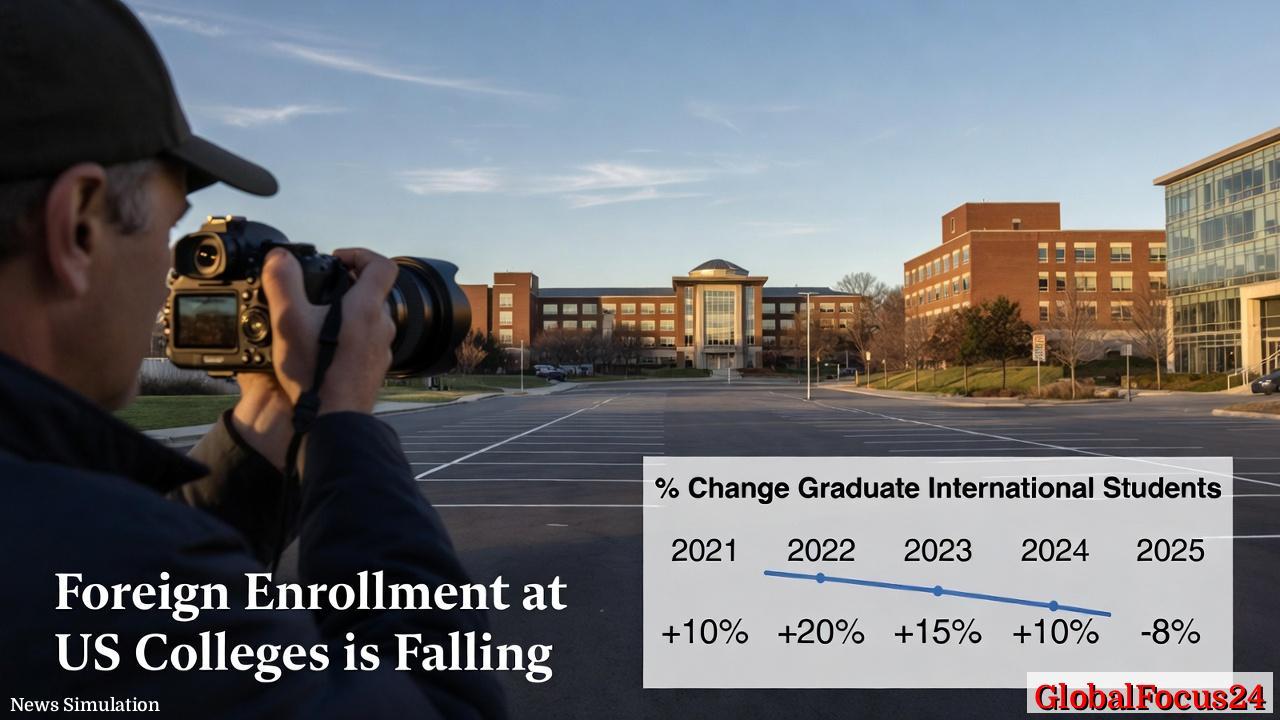

From 2021 through 2024, international graduate enrollment in the United States climbed at an extraordinary pace. After a pandemic-era slump in 2020, numbers rebounded quickly: approximately +10% in 2021, +20% in 2022, +15% in 2023, and another +10% in 2024. By 2025, however, that growth trajectory abruptly shifted to a negative 8%.

This reversal has drawn attention from university administrators and economists alike. For many, it raises questions about the resilience of the U.S. higher education sector in an increasingly competitive global landscape. The decline, while far less severe than the pandemic-driven drops in 2020, is nonetheless the largest one-year contraction in recent memory for graduate international enrollment.

Economic Significance: The Financial Weight of Global Students

International students play a critical role in the financial health of American universities. They contribute billions annually through tuition, housing, research fees, and local spending. The Institute of International Education has previously estimated that international students added more than $35 billion to the U.S. economy in 2024 through direct and indirect contributions.

Graduate students, in particular, often fill essential roles as teaching and research assistants, supporting both academic programs and funded research projects. A 6% decline across this cohort may translate not only to reduced tuition revenue but also to disruptions in laboratory staffing, reduced course offerings, and delays in ongoing research.

Public universities—which typically charge lower tuition for domestic students and rely more heavily on international student fees to maintain budgets—are expected to feel the impact most acutely. A 9% decline in their international graduate ranks could lead to shortfalls in certain departments, particularly in STEM fields, which traditionally attract high proportions of foreign scholars.

Possible Causes: Shifts in Global Mobility and Policy

Although the data report itself did not assign causes, several underlying factors may help explain the downturn. Visa processing delays, rising U.S. living costs, and intensifying competition from other countries have all been cited by educational analysts as contributing influences.

In the years leading up to 2025, Canada, the United Kingdom, Australia, and Germany all implemented streamlined visa policies and immigration pathways for foreign graduates. In contrast, the United States maintained more stringent work authorization requirements and higher living expenses in major cities. These dynamics have gradually tilted the scales for many prospective students comparing global options.

Inflationary pressures in 2024 and 2025 also played a role. Rising housing and healthcare costs, combined with a strong U.S. dollar, made studying in the United States more expensive relative to other destinations. Meanwhile, some foreign governments expanded scholarship programs that specifically favored study within regional partners rather than in the U.S.

Regional and Institutional Variations

The overall national decline masks significant regional differences. Universities in the Midwest and Southeast appeared to weather the downturn better than coastal counterparts, possibly due to lower living expenses and growing investment in research infrastructure. By contrast, institutions in states such as California, Massachusetts, and New York—longtime magnets for international graduate students—saw sharper declines.

Public four-year universities bore the brunt of the losses, with their collective 9% drop far exceeding the national average. Private universities saw smaller reductions and, in some cases, even slight gains in professional schools such as business and law. However, these increases were modest and insufficient to offset the broader graduate enrollment slump.

Smaller colleges and regional universities without global name recognition may be particularly vulnerable if the downturn continues. For many, international students make up less than 5% of total enrollment, yet they contribute disproportionately to research diversity and cultural exchange on campus.

Historical Context: Lessons from Previous Downturns

While the 2025 decline is noteworthy, it is not without precedent. The United States has experienced several short-term dips in international enrollment over the past two decades—most notably after the 2001 terrorist attacks, during the 2008 financial crisis, and amid the 2020 COVID-19 pandemic. Each period reflected broader global disruptions, whether related to security concerns, economic stress, or travel restrictions.

However, previous declines were often followed by strong rebounds, aided by the enduring appeal of U.S. universities and their research ecosystems. The difference in 2025 lies in the structural competition emerging from other nations that have significantly invested in global education strategies. As those countries offer similar academic quality at lower cost or with clearer post-graduation pathways, the traditional U.S. dominance in attracting top graduate talent faces new headwinds.

Broader Implications for the U.S. Research Ecosystem

The decline in graduate international students could have ripple effects far beyond campus enrollment numbers. Graduate students drive much of the research output that underpins scientific and technological innovation in the United States. Foreign students are disproportionately represented in fields such as engineering, computer science, and physical sciences—areas critical to national competitiveness.

A sustained downturn could slow progress in research productivity, reduce the pipeline of skilled professionals in key industries, and even affect university rankings tied to research impact. Some academic leaders have expressed concern that without swift adjustments to visa policies or financial support systems, the U.S. may see talent redirected elsewhere, diminishing its role as a global research leader over time.

Comparing Global Trends

Globally, student mobility continues to expand, but destination preferences are shifting. Canada recorded steady growth in 2025 after easing post-graduation work restrictions, while Australia rebounded strongly from its pandemic-era slump due to aggressive recruitment campaigns. The United Kingdom, though experiencing plateaued numbers, still benefited from favorable migration routes for graduates entering its workforce.

In contrast, the U.S. decline stands out among major education destinations. International applicants once viewed the American graduate system as unmatched in research scope and doctoral funding. Yet recent policy uncertainty, combined with more consistent incentives abroad, is eroding that advantage. The trend mirrors patterns seen in the mid-2010s, when other English-speaking nations temporarily outpaced U.S. growth in international student markets.

Universities’ Responses and Adaptation Efforts

In light of the 2025 figures, universities are moving quickly to adapt. Several institutions have announced renewed international outreach programs, new scholarships targeting high-demand regions such as South and Southeast Asia, and hybrid degree structures that combine remote coursework with shorter in-person residencies to reduce costs.

Others are forming partnerships with overseas institutions to offer joint degrees or research exchanges, aiming to maintain global engagement even if on-campus enrollment falls. These efforts reflect a broader recognition that international education is no longer a one-way flow to the United States—it is now a distributed network of academic mobility.

Public universities, facing greater financial pressure, may need to make budgetary adjustments or reconsider admissions strategies. Some have discussed expanding domestic recruitment for graduate programs, though this is unlikely to fully offset the gap in the near term.

The Outlook for 2026 and Beyond

Analysts caution that one year of decline does not necessarily signal a long-term downturn. Economic stabilization, improved visa processing, and targeted federal initiatives could help restore growth in international graduate enrollment by 2027. However, recovery will depend heavily on how effectively institutions and policymakers address the root causes of the 2025 decline.

If the United States can reinvigorate its appeal to global scholars—through affordability, streamlined policy, and enhanced research opportunities—it may regain its upward trajectory. Without such changes, international students could continue diversifying toward other countries, reshaping the global landscape of higher education for the decade ahead.

For now, the 2025 enrollment drop stands as a clear reminder that even a world leader in education must constantly adapt to remain competitive in a rapidly changing global marketplace.