Hedge Funds’ Exposure to Magnificent 7 Stocks Hits Record High Amid AI Boom

Hedge Funds Increase Bets on Tech Giants

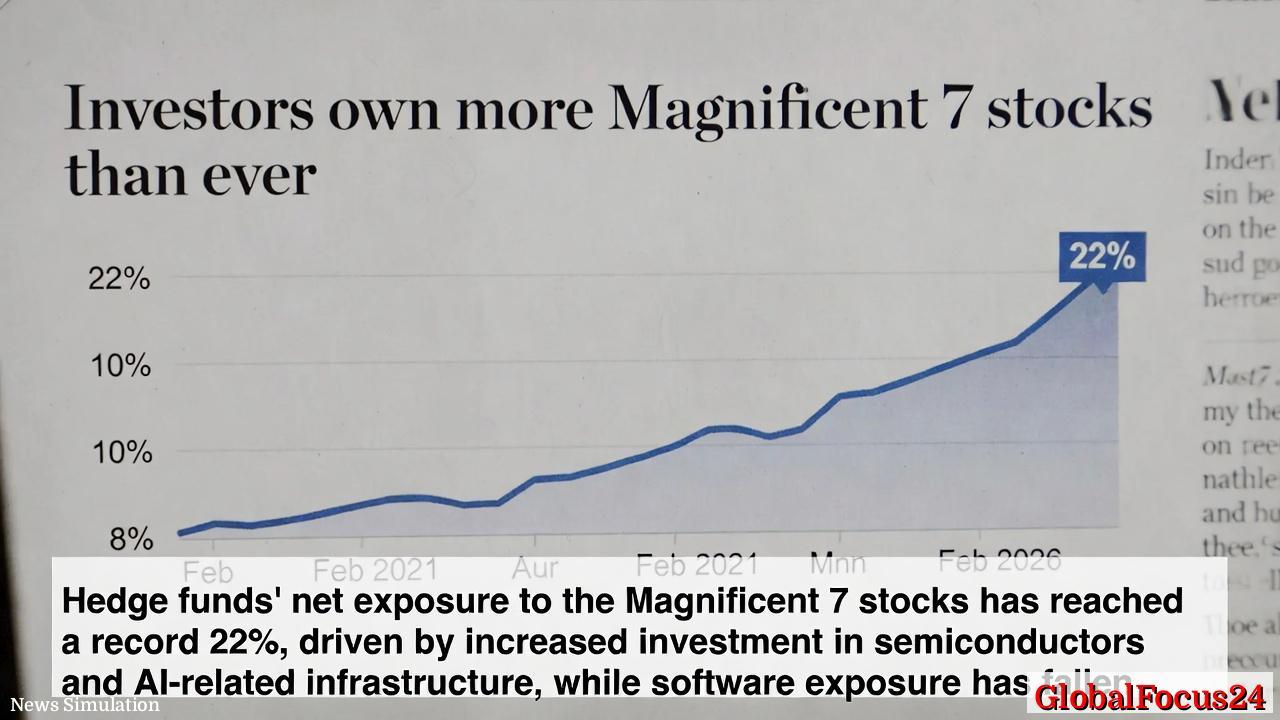

Hedge funds are deepening their commitment to America’s largest technology firms. The combined net exposure to the so-called “Magnificent 7” — a group that includes Apple, Microsoft, Alphabet, Amazon, Meta Platforms, Nvidia, and Tesla — has surged to a record 22% of total U.S. net equity exposure as of February 5, 2026, according to Goldman Sachs Prime Book data. This marks a sharp rise of 10 percentage points since April 2025 and nearly three times the level recorded during the depths of the 2022 bear market.

The move underscores a major shift in hedge fund portfolios toward concentrated bets in the technology sector, largely driven by enthusiasm for artificial intelligence and the hardware that supports it. The 22% figure represents the highest share since data tracking began, capping a five-year trend of rising exposure to large-cap tech leaders that dominate both market capitalization and investor sentiment.

A Decade-Defining Momentum Trade

From a historical perspective, the “Magnificent 7” have become the backbone of U.S. equity performance. Their combined market capitalization now exceeds $14 trillion, representing a significant portion of the S&P 500’s total value. Over the last five years, these firms have redefined market leadership — a pattern reminiscent of the “Nifty Fifty” dominance seen in the 1970s and the dot-com boom of the late 1990s.

The recent surge in hedge fund positioning mirrors broader investor momentum around artificial intelligence. Nvidia, in particular, has seen extraordinary inflows as investors bet on continued demand for AI chips powering data centers, cloud computing, and generative AI platforms. Microsoft and Alphabet have benefited as key providers of AI infrastructure and productivity tools. Apple and Amazon, while less directly involved in AI platforms, remain vital long-term holdings due to their scale and integration across digital ecosystems.

AI Infrastructure and the Semiconductor Rally

While software exposure among hedge funds has declined to a five-year low, allocations to semiconductors and semiconductor equipment have risen to the highest level in the same period. This rotation highlights a structural rebalancing within technology portfolios. The underlying thesis: computing infrastructure is the foundation of the AI economy, while pure software plays face increased valuation scrutiny and slower organic growth.

Semiconductor manufacturers such as Nvidia, Advanced Micro Devices (AMD), and equipment suppliers like ASML and Applied Materials have been key beneficiaries. Industry forecasts suggest global semiconductor sales will surpass $600 billion in 2026, bolstered by surging demand from data centers and AI-enabled devices. Hedge funds appear aligned with this trajectory, treating chipmakers as the “picks and shovels” providers of the AI gold rush.

From Bear Market to Concentrated Bets

The path from the 2022 bear market to today’s record concentration tells an instructive story about institutional appetite for tech. During that downturn, hedge funds reduced exposure to the Magnificent 7 to around 8% of total net U.S. equity exposure, reflecting widespread risk aversion amid rising interest rates and fears of overvaluation. As inflation eased and monetary policy stabilized through 2024 and 2025, fund managers systematically rebuilt tech positions, chasing both earnings resilience and long-term innovation narratives.

The renewed concentration in just seven names is notable for its magnitude and speed. Typically, diversification is a core hedge fund principle aimed at mitigating idiosyncratic risk. Yet in this cycle, diversification has given way to conviction: big-cap tech firms are viewed as safer, more liquid, and more durable growth vehicles than smaller-cap peers. This positioning, however, raises questions about market breadth and systemic vulnerability should these megacaps falter.

Concentration Risks and Market Implications

The record exposure underscores a paradox within today’s equity markets. Hedge funds, by design, seek idiosyncratic opportunities — but their collective positioning often mirrors passive market trends. This herding effect may increase volatility if sentiment shifts. A correction in one or more of the Magnificent 7 could trigger disproportionate de-risking, amplifying market drawdowns.

Historically, concentrated market leadership has preceded periods of uneven returns. The top-heavy structure of the S&P 500 resembles patterns seen before the 2000 dot-com bust and the 2018 FAANG correction. In both periods, a handful of dominant firms drove outsized gains until macro conditions or valuation pressures reversed momentum. Analysts now debate whether 2026 marks another such inflection point or the early stage of a lasting technological supercycle anchored in AI infrastructure.

Comparing Global Equity Concentrations

Regional comparisons reveal stark contrasts. In Europe and Japan, hedge fund exposure remains more evenly distributed across sectors, with a heavier tilt toward industrials, financials, and energy. European equity managers, for instance, maintain less than 10% exposure to their top seven holdings combined, reflecting a broader investment landscape and fewer outsized technology giants.

By contrast, the U.S. market’s structural composition — dominated by a handful of high-growth, high-margin tech firms — naturally funnels capital toward the largest players. The depth of liquidity and scale of U.S. indices amplify this dynamic. Asian markets, particularly South Korea and Taiwan, show elevated exposure to semiconductors but lack equivalently dominant platform companies, making their market concentration sectoral rather than corporate.

Economic Drivers of the 2026 Rally

Several macroeconomic factors have supported the renewed rally in the Magnificent 7 through early 2026. A softer inflation trajectory and a more balanced Federal Reserve policy path have stabilized valuation multiples. Corporate earnings for major tech firms remain robust, supported by AI integration across cloud computing, digital advertising, and consumer devices.

Additionally, the ongoing investment cycle in AI infrastructure — data centers, energy-efficient chips, and large-scale compute clusters — continues to absorb capital. Hedge funds perceive these as multi-year trends, viewing short-term valuation risk as secondary to structural growth potential. Compared with other sectors, technology’s pricing power and scalability offer superior margin resilience amid uncertain global demand.

Capital Rotation and Hedge Fund Strategy

Despite record levels of tech exposure, hedge fund behavior indicates selective rotation rather than wholesale exuberance. While exposure to hardware has grown, positioning in traditional software and consumer internet names has fallen. Managers have also increased hedges in related sectors such as cybersecurity, cloud infrastructure, and digital services to balance portfolio risk.

This nuanced repositioning reflects lessons from previous cycles. Hedge funds remain mindful of crowding risk and algorithmic correlations that can amplify downside moves. Many managers deploy factor-based hedges — such as shorting index futures or pairing growth-oriented longs with defensive holdings — to maintain directional flexibility. Still, the sheer size of institutional capital tied to the Magnificent 7 leaves the broader market sensitive to any shift in their earnings outlook or regulatory environment.

Historical Context and the Path Ahead

The trajectory of hedge fund exposure to major technology stocks marks a profound statement about investor confidence in the U.S. innovation ecosystem. From the 2020 pandemic-era tech surge to the 2022 correction and the resurgence fueled by AI breakthroughs, hedge funds have alternated between caution and conviction. The current peak suggests conviction has decisively returned.

Yet even as hedge funds embrace concentration, history cautions against complacency. Episodes such as the dot-com bubble and the post-2018 FAANG correction illustrate that technological transformation, while real, does not guarantee linear returns. Shifting capital expenditure cycles, regulatory scrutiny, and geopolitical tensions in semiconductor supply chains could all challenge the sector’s momentum over the medium term.

Outlook for 2026 and Beyond

Looking ahead, the central question for the remainder of 2026 is whether the Magnificent 7 can sustain earnings growth that justifies their premium valuations. AI adoption continues to accelerate, but investor enthusiasm has already priced in aggressive long-term projections. If growth moderates or competition intensifies, the record-high hedge fund exposure could become a source of downside pressure.

Still, many analysts view current positioning as rational given the technology sector’s structural advantages: dominant market share, strong balance sheets, and clear exposure to transformative trends such as artificial intelligence, cloud computing, and digital infrastructure modernization. As global capital reorients toward innovation-driven growth, hedge funds may remain tethered to the same megacap names that define modern investing.

For now, data shows a market environment where hedge funds are not just participating in the AI revolution — they are all in. The record 22% exposure to the Magnificent 7 confirms that America’s largest technology companies remain the heartbeat of both Wall Street strategies and global equity performance heading into the middle of the decade.