Global copper demand accelerates as supply tightens: a 2040 outlook for the global metals market

The global copper market stands at a pivotal juncture. Forecasts for the next two decades point to a substantial widening of the demand-supply gap, driven by a confluence of electrification, advanced technologies, and strategic spending across defense and infrastructure. As the world leans into decarbonization, digital transformation, and the broader push toward reliable, high-capacity electrical systems, copper’s role remains central. Yet the supply side faces structural challenges that could redefine pricing, sourcing strategies, and regional competition.

Historical context: copper as the backbone of modern electrification

Copper’s prominence in modern economies dates back to the spread of electrification in the early 20th century and has only intensified with the information age. Its unique combination of high electrical conductivity, ductility, corrosion resistance, and recyclability makes it indispensable for power grids, wind and solar generation, electric vehicles, data centers, and a wide array of consumer electronics.

Over the past two decades, copper demand has grown in step with urbanization and industrial capacity expansion. The late 2000s recovery after the global financial crisis, followed by steady growth in emerging markets, underscored copper’s sensitivity to investment cycles and technological adoption. More recently, the push toward electrification of transportation and the expansion of renewable energy generation have reinforced copper’s status as a critical commodity for both the energy transition and broader economic resilience.

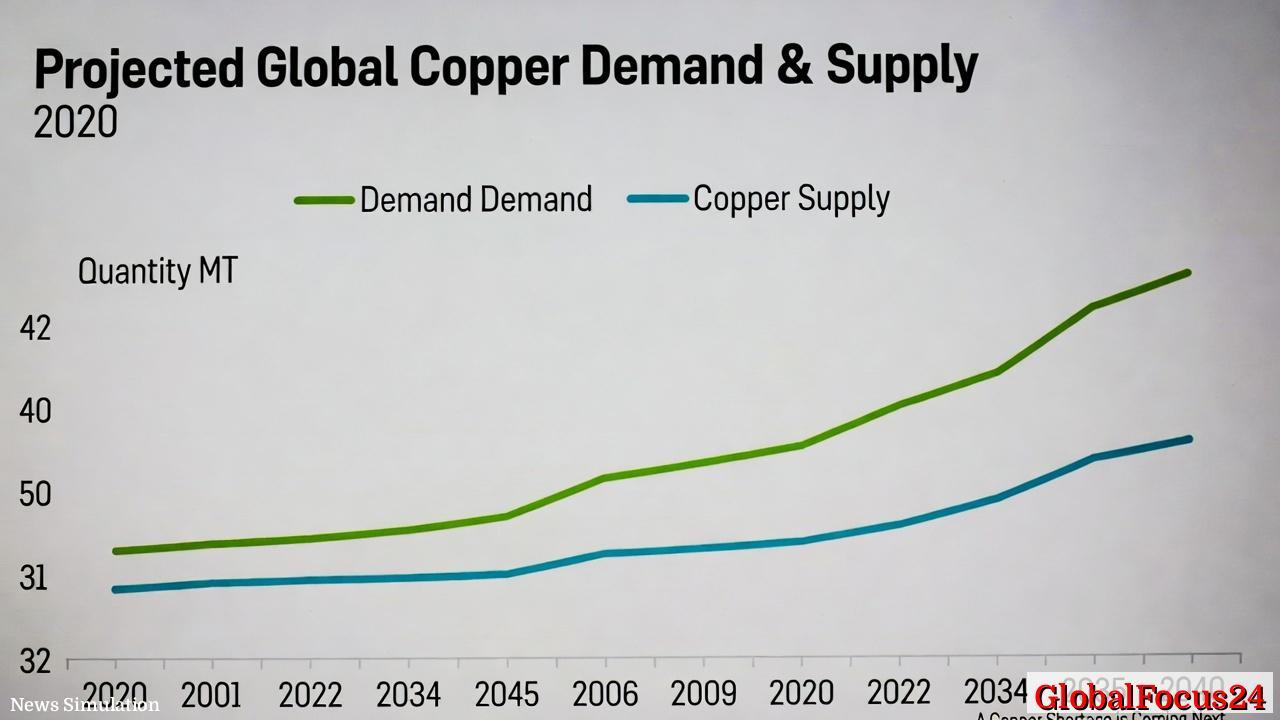

Forecasts for 2040: demand surge versus supply constraints

Industry analyses predict global copper demand to reach about 42 million metric tons by 2040, representing roughly a 50% increase from current levels. This trajectory reflects several structural drivers:

- Electrification of power infrastructure: Upgraded grid infrastructure, expansion of transmission lines, and improvements in grid resilience require substantial copper content, given its efficiency and long service life.

- Electric vehicles and charging networks: EVs, home and commercial charging, and public charging networks embed copper across motors, windings, cables, inverters, and charging hardware.

- Data center growth and digital infrastructure: Hyperscale data centers and 5G/6G networks demand reliable, high-conductivity cabling and power distribution components.

- Defense and strategic technologies: High-performance copper alloys and specialized components support advanced defense systems, aerospace, and critical infrastructure.

On the supply side, copper has a more constrained growth path. Projections indicate mined production could peak and subsequently decline under the current portfolio of committed, probable, and possible projects. Meanwhile, recycled copper scrap is expected to rise significantly, potentially more than doubling to around 10 million metric tons by 2040, reflecting an intensifying emphasis on circular economy practices. Despite this uptick in recycling, the overall supply is forecast to fall short by about 10 million metric tons annually by 2040, creating a substantial gap—approximately 24% below projected demand.

The 2020–2040 trajectory: a widening gap

Historical progression in the forecast shows a clear pattern:

- 2020: Demand and supply hold roughly in balance, each in the mid-20 million tonnes range.

- 2025: Demand edges ahead of supply, with totals near 28–30 million tonnes as electrification and industrial activity accelerate.

- 2030 onward: The gap widens more rapidly as demand climbs toward and beyond 40 million tonnes, while supply plateaus around the 32–34 million tonne mark before trending downward to roughly 31 million tonnes by 2040.

This divergence creates a structural imbalance that has broad implications for manufacturers, policymakers, and regional economies reliant on copper-intensive industries.

Economic impact: pricing signals, investment, and downstream effects

- Price volatility and investment discipline: A persistent supply shortfall tends to support higher copper prices, incentivizing new exploration and development activity but also testing project economics in a high-interest environment. Buyers face longer lead times for concentrate supply and potential contest for refined copper, particularly in markets with ambitious infrastructure and clean-energy agendas.

- Regional competitiveness: Regions rich in copper resources or advanced recycling capabilities could gain a competitive edge. Conversely, regions heavily dependent on copper imports may experience larger trade deficits or heightened exposure to price swings.

- Industry strategies: Utilities, manufacturers, and technology firms may accelerate hedging, stockpiling of refined copper products, and supply-chain diversification. Industries could also invest more in copper recycling infrastructure and product design optimization to minimize material intensity without sacrificing performance. -Policy and infrastructure planning: Governments may prioritize critical minerals strategies, ensure strategic stock reserves, and streamline permitting for copper-related mining and recycling projects. This could influence local employment, regional development, and fiscal budgets.

Regional comparisons: how different districts may be affected

- North America: The United States and Canada have robust copper demand tied to electrical infrastructure modernization, electrified transport initiatives, and data center growth. Domestic copper production and recycling activities could be leveraged to reduce import dependence, though domestic supply expansion may require regulatory certainty and streamlined permitting environments.

- Europe: The EU’s large-scale renewable energy deployment and vehicle electrification programs create strong copper demand drivers. Europe also emphasizes circular economy policies, which could enhance recycling rates and sustained supply. However, competition for refined metal and raw materials could intensify with similar regional priorities among neighboring economies.

- Asia-Pacific: This region represents a significant portion of both global consumption and production. China and other economies in the region are central to copper demand through infrastructure investment, manufacturing, and electronics production. Regional supply dynamics, including mine development, concentrate trade, and refined copper capacity, will influence global price formation and market balance.

- Latin America and Africa: These regions host substantial copper ore reserves and mining activity. Sustainable development, environmental considerations, and commodity price cycles will shape investment flows, local employment, and export revenues. Recycling capacity in these regions is developing, with potential to alter regional supply profiles over time.

Technical and market considerations: drivers of change

- Recycling as a lever: The projected rise in recycled copper supply to about 10 million metric tons by 2040 highlights the role of circular economy practices. Efficient collection, separation, and refining processes will be essential to maximize recycled copper’s contribution to the market, potentially mitigating some supply constraints.

- Smelting and refining capacity: The balance between mine production and metal refinement affects market dynamics. Delays or closures in refining capacity can tighten the market, even in the presence of adequate mine output, underscoring the importance of integrated supply chains.

- Substitution and material science: While copper remains the default choice for many electrical and electronic applications, ongoing research into alternative materials or copper alloy optimization could influence future demand. However, given copper’s unrivaled combination of properties for many high-performance applications, widespread substitution is unlikely in the near term.

Implications for stakeholders

- Utilities and grid operators: To safeguard reliability amid tight copper supply, utilities may pursue long-term procurement strategies, diversify material sourcing, and invest in grid modernization projects with material efficiency in mind.

- Manufacturers and OEMs: Copper-intensive products may see sustained price pressures. Design improvements, modular architectures, and higher recycling content can help manage material costs while maintaining performance.

- Investors and financiers: The 2040 outlook suggests potential opportunities in mining, refining, and recycling ventures, as well as in supply-chain resilience infrastructure. However, capital allocation will depend on project economics, regulatory risk, and geopolitical considerations.

- Policymakers: Copper supply security intersects with energy policy, critical minerals strategies, and climate objectives. Strategic stock mechanisms, investment incentives for mining and recycling, and environmental standards will shape market outcomes.

What to watch next: indicators of approaching peaks and shifts

- Capex cycles in mining and smelting: Sustained investment beyond current project commitments could alleviate some supply constraints, while postponement or cancellations could deepen the gap.

- Recycling efficiency and collection rates: Improvements in recycling infrastructure and scrap recovery could meaningfully alter the supply curve, offering a counterbalance to constrained mined output.

- Demand accelerators: Developments in renewable energy deployment, electric transportation adoption, and data-driven technologies will continue to feed copper demand. Monitoring policy shifts, economic growth trajectories, and technology breakthroughs will help gauge the pace of consumption growth.

- Trade flows and regional dynamics: Shifts in trade policies, tariffs, and regional partnerships can affect copper pricing and availability. Diversified sourcing strategies will likely become more prevalent as buyers seek risk-adjusted supply chains.

Conclusion: planning for a copper-driven future

The copper market faces a clear structural challenge: robust demand growth driven by electrification and technology, paired with a supply outlook that may not keep pace, even with rising recycling contributions. This dynamic is not simply a matter of higher prices; it reshapes industrial planning, investment priorities, and regional development strategies. As nations and companies align their long-term budgets with decarbonization and digitalization goals, copper’s centrality to modern life becomes even more pronounced.

In the coming years, the balance between mined production, refining capacity, and recycled material will determine not only commodity markets but also the resilience of critical infrastructure, the affordability of green technologies, and the pace at which economies can transform toward more sustainable, interconnected systems. Stakeholders across sectors should monitor capacity additions, recycling advancements, and policy developments to anticipate shifts in supply reliability and market dynamics.